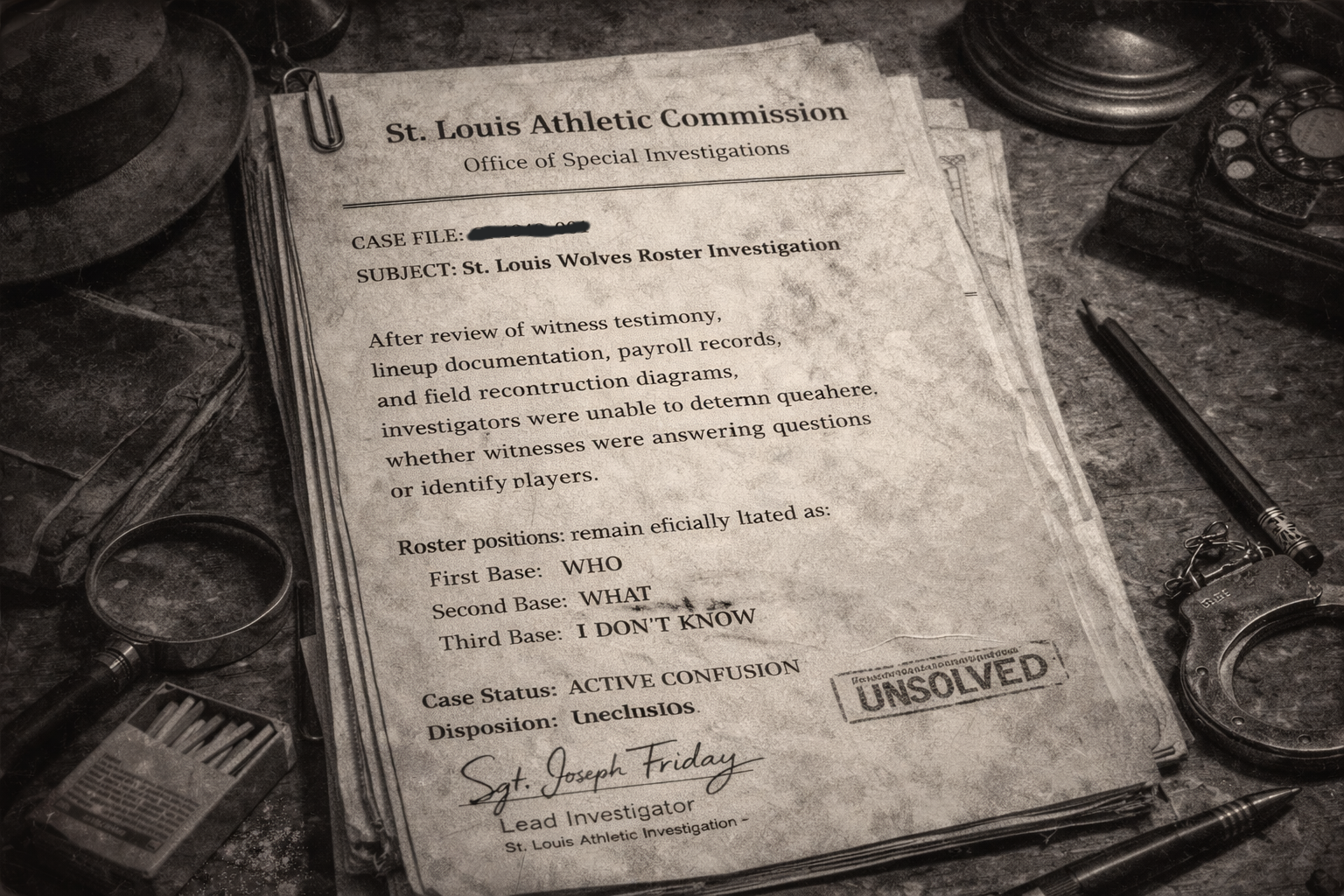

Case File — Who’s on First Investigation

Financial Inquiry — St. Louis Wolves Roster Investigation

Crow University investigators have assembled the following findings after review of recovered archival materials revealed evidence of altered payroll records, missing financial documentation, and unresolved questions regarding the role of Lou Costello.

For decades, public attention remained fixed on a single question: Who’s on first? Investigators now conclude that this line of public fascination may have obscured the more important issue. Based on the surviving record, the central question was not roster confusion. The central question was money.

Recovered ledgers show names written in, erased out, and written over. Multiple entries appear unstable, fabricated, or otherwise unverifiable. The condition of the payroll material prevents any confident determination of who was actually paid.

The surviving evidence further suggests that compensation may have been issued in cash rather than by check. This would have reduced traceability, avoided normal banking oversight, and made it substantially easier to conceal recipients through aliases, substituted identities, or incomplete bookkeeping.

Recovered Exhibits

Investigators identified five principal exhibits associated with the case file.

The Costello References

Investigators note that Lou Costello appears in two separate evidentiary contexts.

First, the Wolves payroll ledger contains a handwritten marginal notation bearing the name Lou Costello. That notation is present in a ledger already marked by erasures, alterations, and apparent instability in the listed identities.

Second, the reconstruction board assembled by the original investigators places Costello’s photograph larger than the others and in a position of clear investigative emphasis. Also visible on the board is what appears to be a payment receipt or disbursement record associated with him.

That receipt has not been recovered in the surviving archive.

The result is two distinct references: one in the altered payroll ledger, and one on the investigators’ board. Neither item by itself conclusively proves that Costello was paid by the St. Louis Wolves or formally played for the club. Taken together, however, they place him unusually close to the financial center of the case.

The Public Story and the Private Ledger

The archival pattern suggests that the public spectacle surrounding roster confusion may have served as a diversion from financial irregularities occurring in the background.

In practical terms, the public argued over names, positions, and absurd exchanges. Meanwhile, the surviving documents show altered payroll records, apparent cash movement, and missing financial support documents.

Under that reading, the confusion was not a byproduct of the case. It may have been part of the mechanism.

Put plainly: Lou Costello may not have been confused at all. He may have been confused like a fox.

Investigative Discontinuity

The reconstruction board indicates that original investigators had developed meaningful leads and had narrowed their attention toward specific persons of interest. Yet no known prosecution followed. No completed financial accounting appears in the surviving record. No final charging action has been found against Abbott or Costello.

That absence raises additional questions about whether the case was pursued to its full extent. The possibility cannot be excluded that evidence was lost, that the matter was allowed to stall, or that enforcement authorities failed to advance the inquiry despite substantial warning signs.

In the opinion of current archival investigators, the surviving record supports inquiry into possible tax evasion, falsification of payroll documents, identity misuse, off-book cash compensation, and potentially coordinated enterprise-level misconduct consistent with what, under a modern framework, might invite racketeering-style scrutiny.

Final Determination

Crow University investigators issue the following summary determination:

The historical question most closely associated with this case was never sufficient to explain the evidence.

The public asked:

Who’s on first?

The recovered record asks something else entirely:

Who handled the money?

Who received the money?

Where did the money go?

Once the ledger is examined, the baseball question collapses. What remains is a cold case involving altered records, unexplained cash practices, missing documentation, and a figure whose name appears both in the margin of the payroll ledger and at the center of the original investigators’ board.

This was never just about who stood on first base.

It was about who took the money.

Related Archival Record

The full reconstruction of the investigation is documented in the official Crow University archival study: